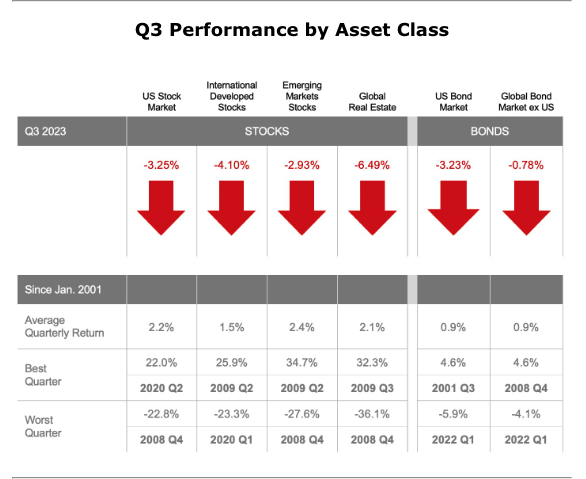

.png)

What is hype, and what is reality?

As investors, we are always asking ourselves this question. In 2021, when over-optimistic traders gave money hand over fist to any startup with a pulse, grocery delivery company Instacart was valued at $39 billion. At the time, it was venture capital-owned with plans for an eventual initial public offering, IPO.

In contrast, Kroger is a national grocer with several regional chains, such as Fred Meyer, Roundie’s, and Ralphs. In 2021, Kroger had a market cap of about $25 billion, meaning Instacart, a deliverer of groceries, was thought to be a more valuable company overall than a large and extremely successful national grocer.

In 2022, Kroger reported over $137 billion in revenue, with a net income of $2.24 billion. Instacart reported about $2.5 billion in revenue and lost $74 million in 2022. These companies are not the same, and yet, at the time, investors in Instacart felt it deserved a significant premium.

Fast forward to 2023, and a different story is told. Instacart completed its IPO in September, and the market valued the company at $10 billion, a nearly 75% decline and a $29 billion haircut from its previous valuation.

Meanwhile, Kroger stock began 2021 at $31.76 per share and is now worth $45.09, a 42% increase over nearly three years. Moreover, the stock kicks out an annual dividend of $1.16, which has grown at an annualized rate of about 15.75% over the past five years.

As Shakespeare reminds us, “All that glitters is not gold.” In investing, we call Instacart a glamour stock. The company is growing rapidly, the stock value has increased dramatically, and other investors seem to value it highly. Therefore, it must continue to go up. It’s a tech darling—a unicorn.

Kroger, meanwhile, is boring. Stodgy. Old school.

And yet, had you had the chance at the beginning of 2021 to buy either company, you would have done well to choose the boring grocer, not the startup.

As investors, we are always tempted to extrapolate recent performance indefinitely into the future. This happens with both poor performance and positive performance. A common mistake among 401k participants is to buy the funds that have outperformed recently. Unfortunately, the statistical concept of mean reversion suggests those same outperformers will likely underperform in other years.

On the other hand, investors are prone to panicking and selling their worst holdings during market downturns, even as the roots of the recovery are already in place.

The cure for this is diversification and regular rebalancing of your investment portfolios.

Diversification forces us away from the horrible mistake of over-concentration. A diversified investor would never have invested too much in an Instacart or even a Kroger, favoring owning the entire market rather than a handful of names. The same can be said about global diversification. You do not want to own too much Japan when the U.K. might outperform or too many U.S. stocks when Canada and Mexico are to perform.

So why doesn’t everyone do it? Proper diversification is hard. Your portfolio owns the outperformers just as well as the underperformers. You are constantly fighting the urge to buy more of the former and sell the latter. Luckily, rebalancing solves this.

Rebalancing forces us not to hold our darlings too dear. It’s hard to say, “That position has done so well for me, so let’s sell it!” Worse, with the proceeds, you will buy this other mutual fund, ETF, or asset class that has underperformed, perhaps dramatically. Rebalancing forces us to move in contrast to our instincts, buying underperformance and selling outperformance. Luckily, that’s the name of the whole game. Buy low and sell high!

We love the technical work of designing a thoughtful and well-allocated investment portfolio that is coordinated with your financial plan and goals. But the real work is in sticking with it, not getting distracted by glitz and glamour, and seeing gold where there is only glitter.

This material is intended for educational purposes only. You should always consult a financial, tax, or legal professional familiar with your unique circumstances before making any financial decisions. Nothing contained in the material constitutes a recommendation for purchase or sale of any security, investment advisory services or tax advice. The information and opinions expressed in the linked articles are from third parties, and while they are deemed reliable, we cannot guarantee their accuracy.