If you're approaching 60 with over $2 million saved and wondering whether that's enough to retire comfortably, the conventional wisdom you're hearing might be keeping you trapped in a high-stress career longer than necessary.

You may hear financial advice that tells you retiring before 65 is risky, that you need $3–5 million saved, or that you must follow rigid withdrawal rules to maintain your lifestyle. But this one-size-fits-all approach completely ignores the unique advantages that come with retiring at 60.

The problem is what I call the "accumulation obsession trap." For decades, the financial industry has conditioned successful pre-retirees to focus exclusively on building ever-larger nest eggs, while completely overlooking the strategic advantages of retiring at 60. This creates a powerful incentive to promote ever-higher savings targets, regardless of whether those targets actually align with your personal retirement readiness.

The result is a generation of high-achieving professionals who delay retirement for years chasing arbitrary benchmarks like $5 million in the bank or 25 times expenses, only to discover too late that accumulation was never the true measure of retirement security. The single-number obsession has become the greatest obstacle preventing successful individuals from confidently transitioning to the retirement they've worked decades to achieve.

The Three Misconceptions Keeping You Working Too Long

There are three fundamental misconceptions that keep high-achieving pre-retirees working unnecessarily past age 60. These beliefs are so deeply ingrained in our financial culture that even sophisticated investors never question them, yet they're responsible for keeping thousands of successful professionals trapped in demanding careers when they could already be enjoying retirement.

Why Age 60 Is the Optimal Retirement Sweet Spot

Retiring at 60 puts you in a unique position that doesn't exist at any other stage of life. Three distinct advantages converge at this age.

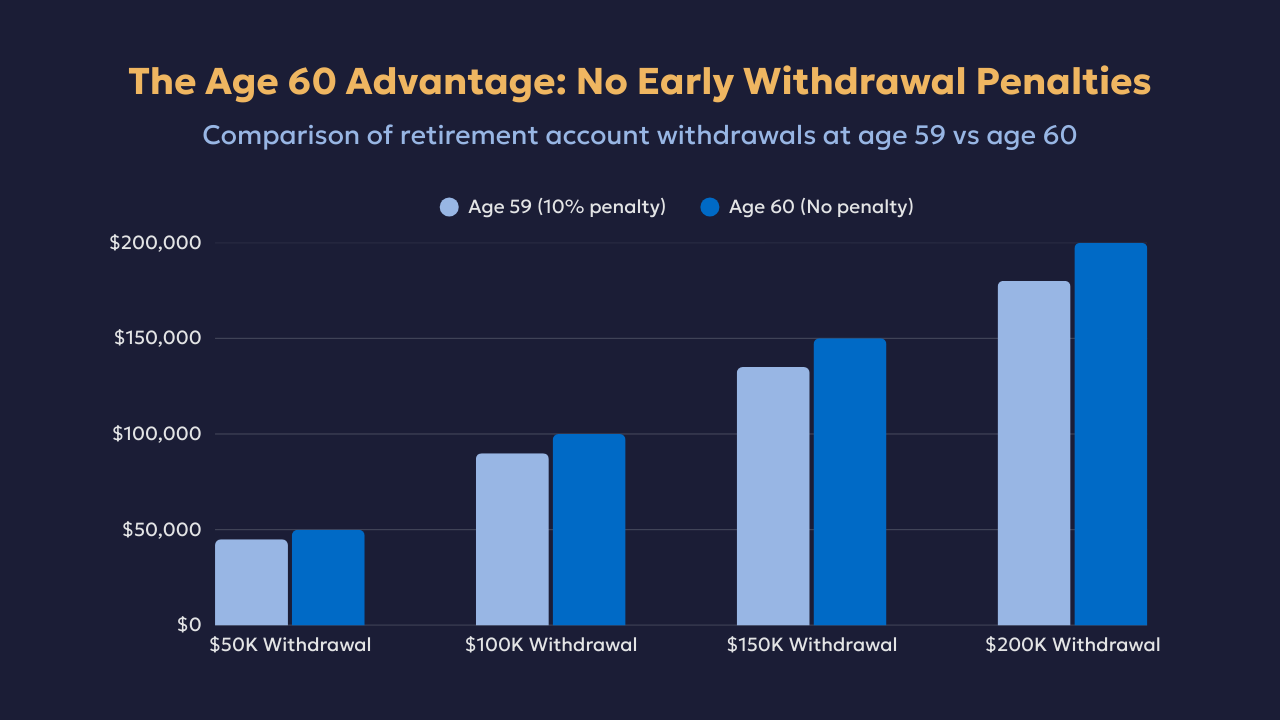

Penalty-Free Retirement Account Access

Unlike retiring at 55 or 57, where you face a 10% early withdrawal penalty, once you hit 59½ that penalty disappears. For every $100,000 you withdraw, you save $10,000 in penalties compared to retiring even slightly earlier, a meaningful advantage that compounds across your full retirement.

You're Young Enough to Truly Enjoy Retirement

Research from the Center for Retirement Research shows that affluent retiree spending follows what's called the "retirement smile" — higher spending in early retirement for travel, second homes, and experiences; lower spending in the middle years; and then potentially higher spending for healthcare later on. By retiring at 60, you maximize the golden years when you have both the health and the energy to enjoy your wealth.

A Strategic Five-Year Bridge to Medicare

While you'll need private health insurance until age 65, your wealth gives you access to excellent coverage options. Many successful retirees at 60 can secure comprehensive platinum-level plans or even concierge medicine arrangements that provide superior care to traditional employer coverage.

The Real Math: Why Conservative Rules Don't Apply to You

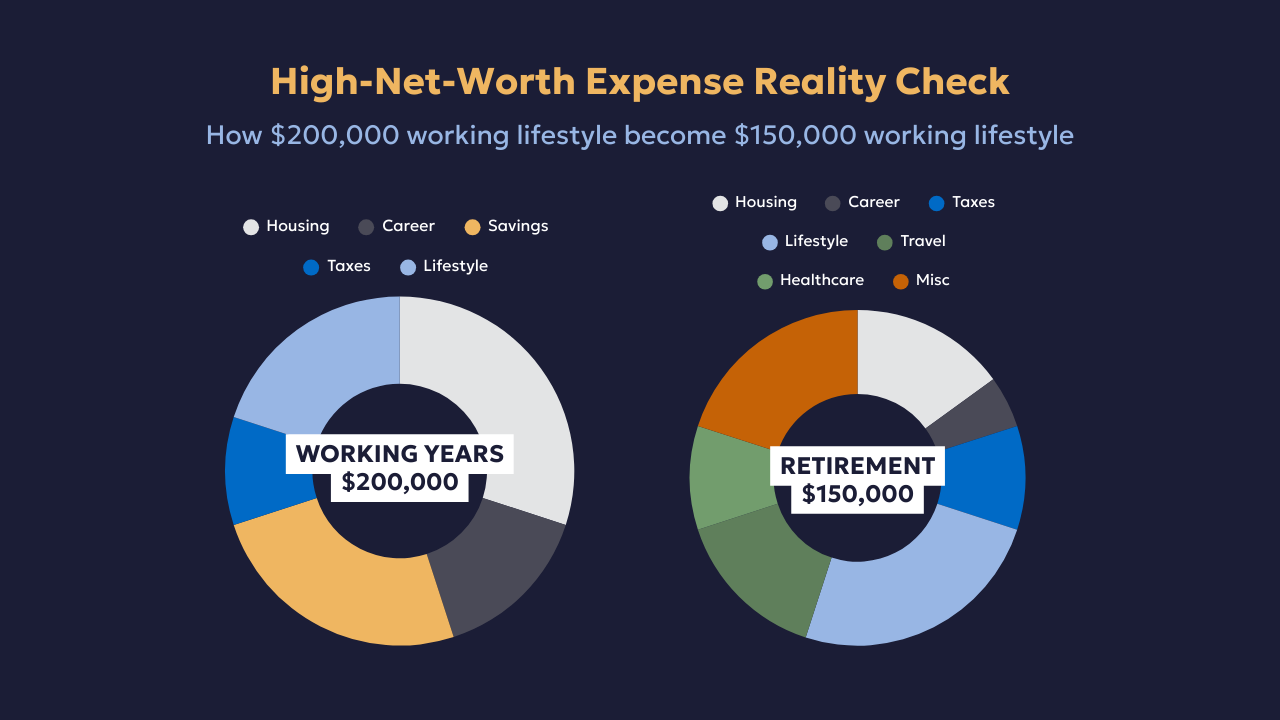

Many advisors serving affluent clients apply conservative rules like needing 25 times your annual expenses or maintaining spending at no more than 3.5% of your portfolio. For someone with a $200,000 lifestyle, that suggests needing $5–6 million. But this completely ignores how retirement actually works for successful individuals.

Even affluent retirees see significant expense reductions. Your mortgage on your primary residence is likely paid off. Your children's college expenses are behind you. You're no longer maximizing 401k contributions or paying FICA taxes. And many of your highest expenses were career-related: expensive business wardrobes, frequent dining out due to long work hours, stress-relief expenditures.

When you account for these changes, that $200,000 working lifestyle might only require $150,000 in retirement to maintain the same quality of life.

Social Security provides an additional foundation on top of that. Even for high earners, the benefits are significant. A successful professional claiming at 62 might receive $30,000–$35,000 annually, and a high-earning couple could see $50,000–$60,000 combined. While this represents a smaller percentage of total income for affluent retirees, it still provides meaningful portfolio protection.

The gap you need to fill from savings drops from $200,000 to perhaps $100,000–$120,000 per year. With $2.5 million invested, that represents a 4–4.8% withdrawal rate, well within the range of sustainable retirement spending, especially with the flexibility that wealth provides.

The Social Security Question: Should High Earners Wait?

A common objection from affluent clients is that Social Security is such a small part of their income that they should simply maximize it by waiting. The conventional wisdom for high earners says to always delay Social Security to maximize your monthly benefit since you don't "need" the money.

Sophisticated research tells a different story. Even for affluent retirees, claiming Social Security early can be the optimal strategy when you consider total portfolio preservation.

When you have guaranteed income flowing from Social Security starting at 62, you reduce the sequence-of-returns risk that threatens early retirees. During market downturns like 2008 or 2020, you're not forced to sell investments at depressed prices to fund your lifestyle. Your portfolio can recover while you live partially on guaranteed income.

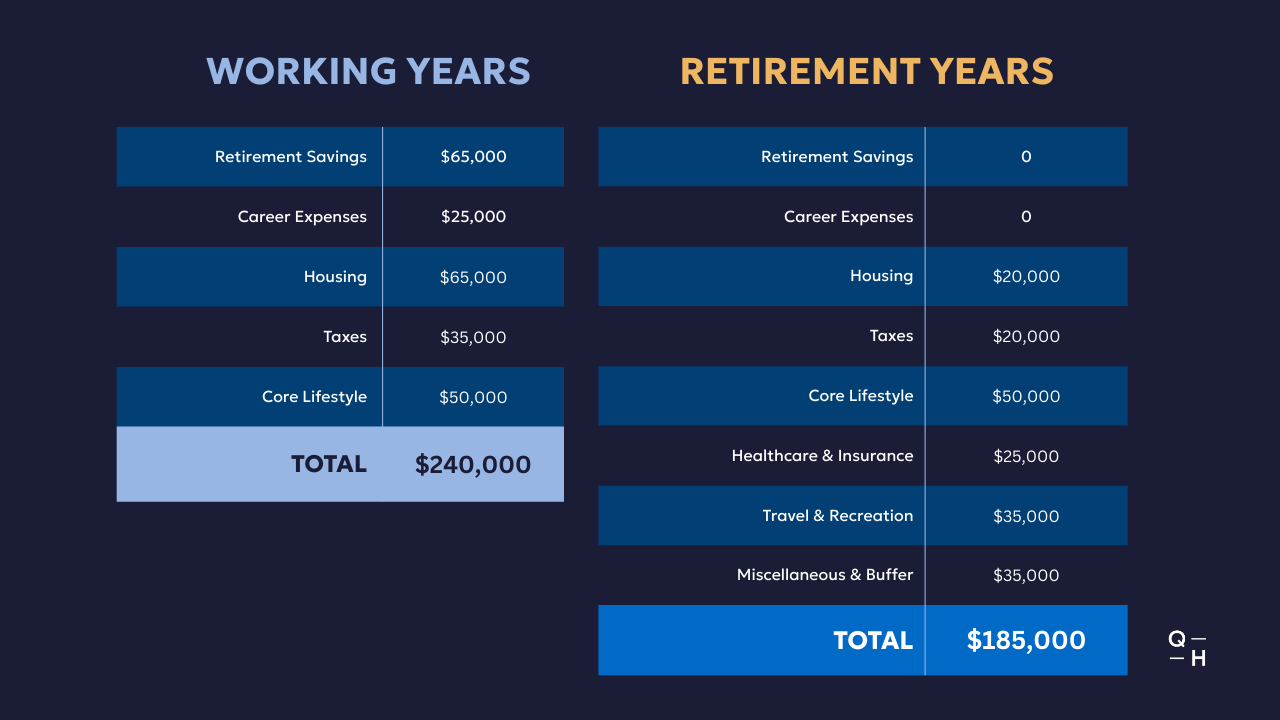

A real client example illustrates this. A couple with $3.2 million felt they needed another $800,000 before they could retire because they were focused on the 4% rule and their $240,000 lifestyle. When we factored in Social Security at 62 providing $55,000 annually, they only needed $185,000 from their portfolio. Using a flexible withdrawal strategy and dynamic spending adjustments, they could safely maintain their lifestyle while actually reducing portfolio risk.

The Four-Step Process to Know If You Can Retire at 60

Here is the proven process we use with high-net-worth clients to determine whether they're truly ready to retire at 60.

Step 1: Analyze Your True Retirement Expenses, Not Your Working Income

Separate essential lifestyle expenses from career-related costs and wealth-building activities. Many successful professionals discover their core lifestyle costs are 20–30% lower than their working-year expenses once they remove business dining, professional development, and aggressive savings contributions.

Step 2: Optimize Your Guaranteed Income Sources

While Social Security may represent a smaller percentage of your income, it still provides valuable portfolio protection. Consider pension benefits, rental income, or other guaranteed sources. The goal is creating a floor of security that allows your portfolio to weather market volatility.

While Social Security may represent a smaller percentage of your income, it still provides valuable portfolio protection. Consider pension benefits, rental income, or other guaranteed sources. The goal is creating a floor of security that allows your portfolio to weather market volatility.

Step 3: Build Multiple Flexibility Levers Into Your Plan

Affluent retirees have unique advantages that most retirement calculators ignore: the ability to adjust discretionary spending during market downturns, potential income from part-time consulting, and geographic arbitrage through seasonal residences. Also consider health savings accounts, Roth conversion opportunities, and tax-loss harvesting strategies that become more valuable in retirement.

Step 4: Implement Sophisticated Withdrawal and Tax Strategies

Use tax location optimization, holding tax-inefficient investments in retirement accounts while keeping tax-efficient investments in taxable accounts. Implement Roth conversion ladders during low-income years before Social Security begins. Consider donor-advised funds for charitable giving efficiency and qualified charitable distributions from your IRAs.

The Bottom Line: Time Is the Real Risk

Retiring at 60 with $2+ million is something thousands of successful professionals could do, and for many it may be the smartest wealth preservation and lifestyle decision available to them. You avoid the 10% early withdrawal penalty that plagues earlier retirement. You maximize your healthy, active years when you can truly enjoy your wealth. And you have a strategic five-year window to optimize your tax situation before Medicare and required distributions begin.

The biggest risk for successful individuals is not running out of money. It's running out of time and health to enjoy the wealth they've accumulated. Every month you delay could be costing you precious years of freedom, travel, and experiences that money simply can't buy back later.

By analyzing your true retirement expenses, strategically leveraging all income sources, and implementing sophisticated withdrawal strategies, you likely already possess everything you need to retire with confidence at 60.

The biggest obstacle for most successful professionals isn't their finances — it's having someone help them see clearly what they've already built. To get a clear picture of your own retirement readiness, schedule an introductory call with us.

Kyle Moore is a CERTIFIED FINANCIAL PLANNER™ professional and founder of Quarry Hill Advisors. Quarry Hill specializes in helping pre-retirees navigate the retirement transition with comprehensive, tax-efficient planning strategies.

-A note from Kyle Moore, CFP®

This material is intended for educational purposes only. You should always consult a financial, tax, or legal professional familiar with your unique circumstances before making any financial decisions. Nothing contained in the material constitutes a recommendation for purchase or sale of any security, investment advisory services or tax advice. The information and opinions expressed in the linked articles are from third parties, and while they are deemed reliable, we cannot guarantee their accuracy.