What Is IRMAA and Why Does It Catch Retirees Off Guard

You spent your career building a retirement portfolio. You have been diligent about Roth conversions, timed your Social Security carefully, and followed every guideline in the financial planning world. Then Medicare sends you a bill that is three times what your neighbor pays. Not because you chose a worse plan. Not because you have more health conditions. Because you made too much money two years ago.

That surcharge is called IRMAA, the Income-Related Monthly Adjustment Amount, and it quietly drains thousands of dollars from high-earning retirees every year. Most people have no idea it exists until that first bill arrives.

In this post, I want to walk through three IRMAA issues that trip up even well-prepared retirees, show you exactly how each one works, and explain what strategic planning looks like to reduce or avoid them entirely.

Issue 1: The Two-Year Time Delay

The first issue is the one that makes IRMAA fundamentally different from almost any other cost in retirement. It operates on a two-year lookback. Your Medicare premiums for 2026 are based on your modified adjusted gross income from 2024, not 2025, not 2026. Two years ago.

So if you did a large Roth conversion in 2024, sold a property, or had an unusually high income year for any reason, you will see that reflected in your Medicare premiums starting in 2026. And in most cases, by the time you receive the determination notice, the income is already locked into your tax return and there is nothing you can do about it.

Here is what the 2026 IRMAA brackets look like for a married couple filing jointly:

These are not gradual increases. They are cliff thresholds. One dollar over the line triggers the full surcharge for the entire tier. At the highest bracket, a couple can pay over $16,500 per year in Part B premiums alone, compared to just under $4,900 at the standard rate. That is a difference of more than $11,600 per year.

A family friend of mine did a large Roth conversion at age 63, a smart move for long-term planning. But the conversion pushed their 2024 MAGI over $310,000. Two years later in 2026, their combined Part B and Part D surcharges added up to an additional $8,400 for the year. Their financial advisor had no idea it was coming either. The conversion itself was the right strategy. The timing and the amount were the problem.

Issue 2: The Conversion Collision

The second issue is what I call the conversion collision. It is the conflict between two fundamentally sound retirement strategies that can become expensive when they overlap.

Roth conversions are one of the most powerful tax planning tools available to retirees. You move money from traditional IRA accounts to Roth accounts, pay taxes at today's rates, and enjoy tax-free growth and withdrawals for the rest of your life. For most high-income retirees, the question is not whether to do Roth conversions. It is how much and when.

The problem is that every dollar you convert gets added to your MAGI for that year, and that MAGI is exactly what determines your IRMAA surcharges two years later.

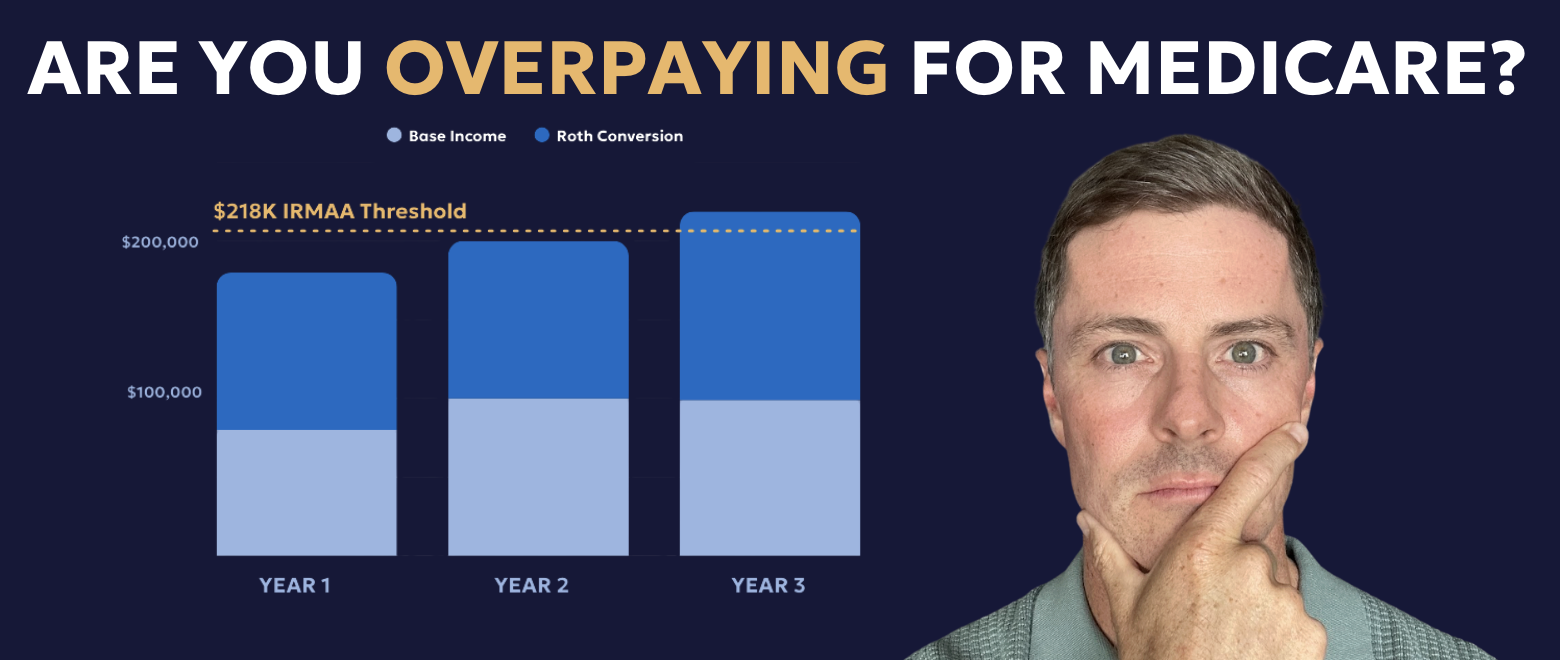

Here is a scenario that plays out more often than people realize. You are 64 and recently retired with $1.4 million in a traditional IRA. Your base income from investments and a small pension is $80,000. You are comfortably below the IRMAA threshold. Your advisor recommends converting $100,000 per year to Roth, pushing your MAGI to $180,000. Still below the $218,000 married filing jointly threshold.

The next year, your investments produce $20,000 more in capital gains than expected. Now you are at $200,000. Still under, but barely.

The year after that, you convert $120,000 because there is room in a favorable tax bracket. Your MAGI is $215,000. Safe by $3,000. But then you realize you forgot to account for a $4,000 capital gain distribution from a mutual fund. Your actual MAGI is now $219,000. One thousand dollars over the threshold, and that single overage triggers nearly $2,000 in additional Medicare premiums for you and your spouse for the entire following year.

This is the conversion collision. The Roth conversion strategy and the IRMAA threshold are working against each other, and because the brackets operate as cliffs rather than gradual increases, small miscalculations create disproportionate costs.

The approach we use at Quarry Hill is to map IRMAA brackets alongside tax brackets every year between retirement and age 73. We identify the maximum conversion amount to stay below the nearest IRMAA cliff, accounting for all income sources including capital gains, distributions, and interest income. Most of our clients find that converting slightly less each year across more years produces a better net outcome than aggressive conversions that trigger surcharges. And here is the detail that most conversion calculators miss entirely: if surcharges hit across multiple years, a couple paying an extra $3,000 per year for five consecutive years has spent $15,000 to $20,000 that never appeared in any conversion tax calculation.

Issue 3: The RMD Cascade

The third issue is the RMD Cascade, and this is where IRMAA can shift from a temporary problem to a permanent one.

Starting at age 73, the IRS requires you to withdraw a minimum percentage of your traditional IRA and 401k balances every single year. These required minimum distributions are taxable income and count toward your MAGI for IRMAA purposes. They are going to happen whether you need the money or not.

The cascading effect works like this. A well-constructed portfolio may continue growing even as you take withdrawals. If your IRA grows at 6% but you are only withdrawing 3.7%, the balance is still increasing year over year. Which means next year's RMD will be larger. Which means more MAGI. Which means higher IRMAA brackets.

I worked with a couple, Tom and Barbara, who hit age 73 with $2.1 million in combined traditional IRAs. Their first year RMDs totaled $79,000. Combined with Social Security and a pension, their MAGI was $185,000, below the IRMAA threshold for married couples.

By age 78, even after five years of withdrawals, their IRA balances had grown to $2.3 million due to market returns. Their RMDs had increased to $107,000. Their combined MAGI was now $252,000, pushing them into the second tier of IRMAA and adding approximately $5,000 per year in surcharges. By age 82, their RMDs were $138,000 per year and they were in the third IRMAA tier, with surcharges costing over $9,000 annually.

Unlike Roth conversions, RMDs are not discretionary. Once they start, you cannot opt out.

What Strategic IRMAA Planning Actually Looks Like

Those are the three issues. Each one independently costs retirees thousands of dollars. Combined, they can drain $20,000 to $30,000 per year from your retirement income, money that could fund travel, time with family, or charitable giving.

The good news is that when you understand these issues, you can plan around them, and in many cases significantly reduce or eliminate IRMAA surcharges entirely.

Build a multi-year income map. This means projecting income from every source, Social Security, pensions, investment income, RMDs, and planned Roth conversions, from now through age 85 and beyond. Then overlay the IRMAA thresholds on that map. The goal is to identify which years have income safely below the thresholds, which years are at risk of crossing a cliff, and how much room exists for discretionary income like conversions.

Time conversions to avoid IRMAA cliffs. The optimal conversion window for most clients is between retirement and age 73, specifically the years when income is lowest. But within that window, conversion amounts need to be calibrated to IRMAA thresholds, not just tax brackets. Sometimes the right conversion amount for a given year is $95,000 instead of $110,000, even though the tax bracket would accommodate more, because that extra $15,000 would push you over an IRMAA cliff. We also recommend finalizing conversion amounts in Q4, ideally September through November, when you have a clear picture of the year's actual income. Converting in January leaves too much uncertainty about capital gains, dividends, and other income that will flow in throughout the year.

Use Qualified Charitable Distributions to reduce the RMD cascade. If you are age 70½ or older and charitably inclined, QCDs are one of the most powerful IRMAA tools available. A QCD allows you to donate up to $111,000 per year directly from your IRA to a qualified charity. The donation satisfies your RMD requirement but does not count toward your MAGI.

Going back to Tom and Barbara: if they donated $40,000 per year through QCDs instead of taking that amount as regular RMD income, their MAGI would drop from $252,000 to $212,000, moving them from the second IRMAA tier back below the threshold entirely. The $40,000 they would have donated to charity regardless saves them nearly $5,000 in annual Medicare surcharges. That is effectively a 12% bonus on their charitable giving.

Know when and how to appeal. If you experience a life-changing event, retirement being the most common for our clients, you can file Form SSA-44 to request that the Social Security Administration reduce your IRMAA surcharges. The form allows you to use a more recent year's income instead of the standard two-year lookback. For someone who retired in 2025 after earning $300,000, their 2024 MAGI would trigger a significant surcharge in 2026. But if their 2025 income dropped to $80,000 after retiring midyear, they can file the SSA-44 and ask Social Security to use the lower figure. Processing takes 30 to 60 days and any overpaid premiums are reimbursed. We have personally helped many clients file for this exception.

The Difference Between Paying and Planning

If you have accumulated $1.5 million or more in retirement, IRMAA is not a minor footnote in your financial plan. It is a significant ongoing cost that interacts with every major retirement decision you make.

The two-year time delay means you need to plan income three years ahead, not react to bills as they arrive. The conversion collision means your Roth strategy needs to account for Medicare costs, not just tax brackets. And the RMD cascade means that without proactive planning, your Medicare surcharges will grow every year for the rest of your life.

The difference between retirees who pay tens of thousands in unnecessary surcharges and those who minimize or avoid them entirely comes down to planning. Specifically, having a systematic process that coordinates income timing, conversion strategy, and withdrawal sequencing with full awareness of the IRMAA thresholds.

That is exactly why we built the Bedrock Planning Process at Quarry Hill Advisors. IRMAA planning is one piece, but it has to be coordinated with your overall tax strategy, your Roth conversions, your withdrawal sequencing, and your estate plan. The Bedrock Process organizes all of this into focused seasons throughout the year so that nothing falls through the cracks and every opportunity is identified.

If you are curious about how the Bedrock Process would apply to your specific retirement situation, click the link in the description to learn more and consider scheduling a retirement readiness assessment. We will walk through your numbers, your goals, and show you exactly where you stand.

-A note from Kyle Moore, CFP®

This material is intended for educational purposes only. You should always consult a financial, tax, or legal professional familiar with your unique circumstances before making any financial decisions. Nothing contained in the material constitutes a recommendation for purchase or sale of any security, investment advisory services or tax advice. The information and opinions expressed in the linked articles are from third parties, and while they are deemed reliable, we cannot guarantee their accuracy.