You're a senior director at a Fortune 500 company. Household income around $280,000. You're maxing out your 401(k), maxing out your HSA, doing everything right. Then you try to contribute to a Roth IRA, and the IRS says no.

You're not alone. Most high-income earners hit this wall and assume a Roth IRA simply isn't available to them. But there's a completely legal two-step process called the backdoor Roth IRA that bypasses the income limits entirely. The catch is that one common mistake can cost you over $2,000 in unexpected taxes if you don't know what to watch for.

This guide walks through the full process and how to get it right.

The Income Limit Problem

In 2026, you can contribute up to $7,500 to a Roth IRA if you're under 50, or $8,600 if you're 50 or older. But only if your income falls below certain thresholds.

For most corporate executives and high-earning professionals, these limits are in the rearview mirror. In 2010, Congress removed income limits on Roth conversions while keeping them on direct contributions. That gap in the rules created the backdoor route.

What Is a Backdoor Roth IRA?

A backdoor Roth IRA is not a different type of account. It's a strategy that uses existing IRS rules in a specific sequence.

A backdoor Roth IRA is not a different type of account. It's a strategy that uses existing IRS rules in a specific sequence.

Step 1: Make a non-deductible contribution to a traditional IRA. There are no income limits for this. At your income level, you won't get a tax deduction, so you're putting in after-tax dollars.

Step 2: Convert that traditional IRA to a Roth IRA. The IRS allows anyone to convert regardless of income. Since you already paid taxes on the contribution, the conversion is generally tax-free.

The result: You've effectively made a Roth IRA contribution even though your income is above the limit. The IRS clarified in 2018 that this strategy is fully legal and acceptable.

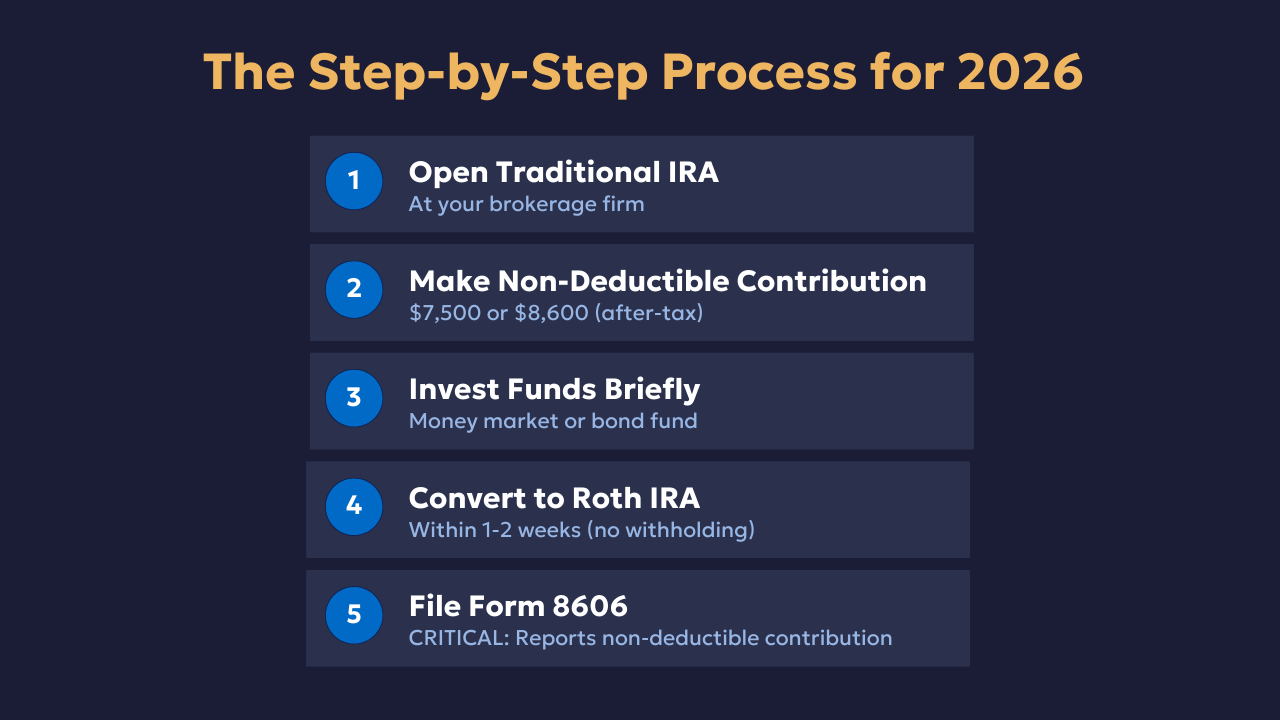

The Step-by-Step Process for 2026

Step 1: Open or Use Your Traditional IRA

You need a traditional IRA account at your brokerage. If you don't have one, open one. Most firms are familiar with this process.

Step 2: Make Your Non-Deductible Contribution

Contribute up to $7,500 (under 50) or $8,600 (50 or older). This is an after-tax contribution. Mark it clearly as non-deductible for your tax records. This is not always clearly shown to CPAs and can be tricky to handle correctly in TurboTax. Having a professional review this step is worth it.

Step 3: Invest the Funds Briefly

Park the money in a money market fund or short-term bond fund. You're not leaving it there long. This step shows the IRS you're treating the traditional IRA as a legitimate account, not just a pass-through.

Step 4: Convert to Roth IRA

Log into your brokerage account and convert from traditional to Roth IRA. Every major brokerage offers this feature. Choose not to withhold taxes since you're converting after-tax contributions. The IRS does not require a waiting period, but waiting a week or two is a reasonable precaution.

Step 5: File Form 8606

This is critical. When you file your taxes, include IRS Form 8606. This form reports your non-deductible contribution and proves you already paid taxes on the money. Without it, you could be taxed twice on the same dollars.

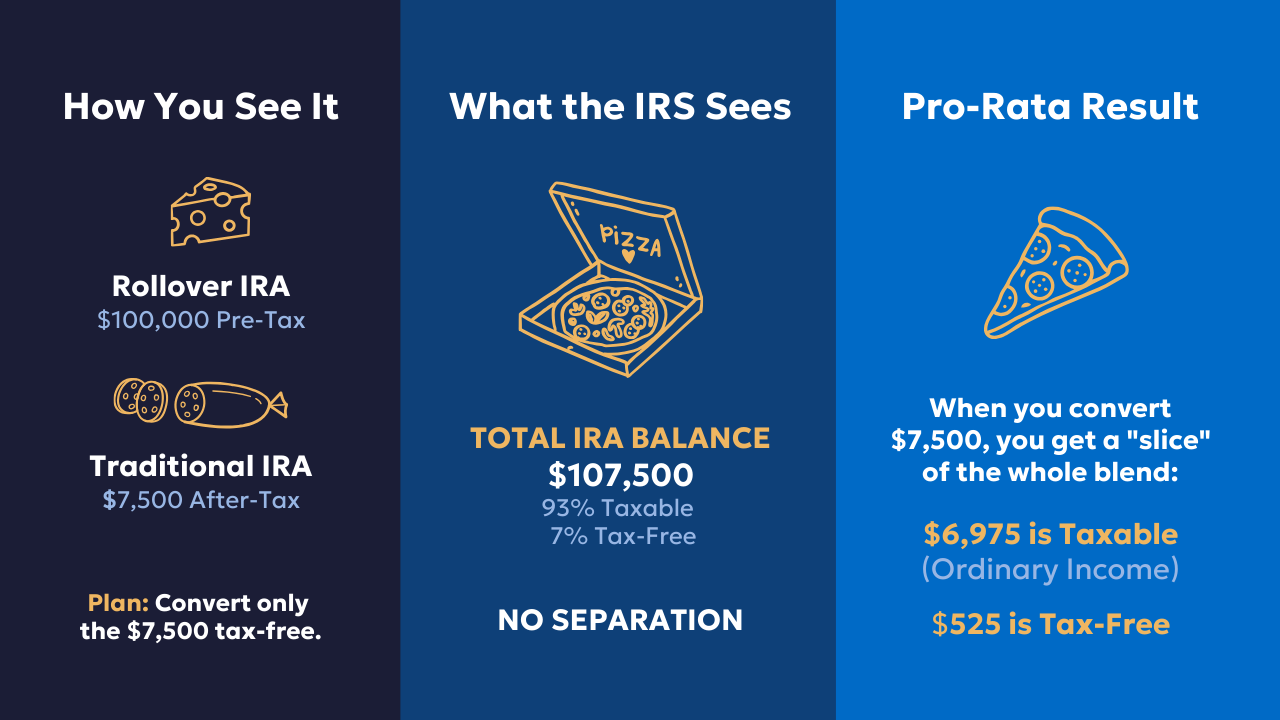

The Pro-Rata Rule: The Biggest Mistake

This is the part that catches people off guard, and it's the single most important thing to understand before you start.

The IRS does not let you pick and choose which IRA dollars you're converting. They treat all of your traditional IRAs, SEP-IRAs, and SIMPLE IRAs as one aggregated account.

Here's what that looks like in practice:

You have $100,000 in a rollover IRA from an old 401(k). All pre-tax money. You contribute $7,500 to a new traditional IRA as a non-deductible contribution.

Your total IRA picture:

- Rollover IRA: $100,000 (pre-tax)

- Traditional IRA: $7,500 (after-tax)

- Total: $107,500

When you convert that $7,500, the IRS applies this formula:

Tax-Free Percentage = $7,500 / $107,500 = 6.98%

Only 7% of your conversion ($525) is tax-free. The other 93% ($6,975) is taxable as ordinary income. That defeats the entire purpose of the strategy.

This happens because people forget about other IRA money they hold elsewhere, or don't realize it counts toward the calculation.

How to Avoid the Pro-Rata Rule

Solution 1: Roll Your IRA into Your Current 401(k)

This is the most commonly recommended approach. Roll your rollover IRA or traditional IRA into your current employer's 401(k) before executing the backdoor Roth. 401(k) balances do not count toward the pro-rata calculation, only IRA balances do. Once your IRA balance is zero, your $7,500 contribution converts 100% tax-free. Check with your plan administrator to confirm your plan accepts incoming rollovers.

One thing worth knowing: some financial advisors charge fees on IRA assets but not on 401(k) assets. If your advisor hasn't brought up this option, it's worth asking why.

Solution 2: Convert Everything

If your plan doesn't accept rollovers, consider converting all your traditional IRA money to Roth at once. You'll pay taxes on the pre-tax portion, but you'll clear the deck for clean backdoor conversions going forward.

Solution 3: Start Fresh

If you're planning ahead, avoid rolling old 401(k)s into IRAs in the first place. Keep them in the old plan or roll them to a new employer's plan. This keeps your IRA clean for future backdoor conversions.

The Step Transaction Doctrine

You may come across warnings about the "step transaction doctrine," a legal principle that says if you execute multiple legal steps to accomplish something otherwise prohibited, the IRS can treat it as a single prohibited transaction.

In practice, the IRS clarified in 2018 that there is no required waiting period between contribution and conversion, and this strategy is legal and acceptable. Waiting a week or two between steps is a reasonable precaution, but the pro-rata rule is a far bigger concern. That's where your attention should be focused.

Case Study: How Sarah Saved $2,000 in Unexpected Taxes

Sarah is a Target senior director earning $195,000. Her household income is $280,000, well above the $252,000 limit. She's maxing out her 401(k) and HSA and wants to save more for retirement.

Her problem: an $85,000 rollover IRA from a previous employer. All pre-tax money.

If she had contributed $7,500 and converted without addressing that rollover:

- Total IRA balance: $92,500

- Tax-free percentage: 8.1%

- Unexpected tax bill: approximately $2,021

Instead, Sarah rolls her $85,000 IRA into her Target 401(k). Her IRA balance drops to zero. She contributes $7,500 as a non-deductible contribution, waits a week, and converts it to Roth. The conversion is 100% tax-free.

Her husband does the same. Together they move $15,000 into Roth accounts annually. Over 20 years at a 7% return, that's over $615,000 in combined Roth assets, available completely tax-free in retirement.

Key Tips to Keep in Mind

Contribution deadlines: You can make 2026 IRA contributions until April 15, 2027. Contributing earlier gives the money more time to grow.

Both spouses can participate: Even if only one spouse has earned income, both can execute backdoor Roth conversions. That's $15,000 or more annually going into Roth accounts.

December 31 matters: The pro-rata calculation uses your IRA balance as of December 31 of the conversion year. Complete any rollovers to your 401(k) before year-end.

This is an annual strategy: Repeat every year. Many clients have been doing this consistently since 2010.

Five-year rule: Each conversion carries a five-year holding period. Not an issue for long-term retirement savings, but worth knowing if you think you might need the funds sooner.

Mega Backdoor Roth: If your 401(k) allows after-tax contributions and in-service distributions, you may be eligible to move $25,000 to $47,500 or more into Roth accounts annually. It's more complex, but worth exploring if the option is available to you.

Your Next Steps

The backdoor Roth IRA is one of the most valuable strategies available to high-income earners. It's legal, IRS-approved, and repeatable every year. But the pro-rata rule can turn a tax-free conversion into a costly taxable mess if you go in without a full picture of your IRA accounts.

If you have questions about how this fits into your overall financial plan, click here to schedule an introductory strategy session with our team at Quarry Hill Advisors.

-A note from Bjorn Amundson, CFP®

This material is intended for educational purposes only. You should always consult a financial, tax, or legal professional familiar with your unique circumstances before making any financial decisions. Nothing contained in the material constitutes a recommendation for purchase or sale of any security, investment advisory services or tax advice. The information and opinions expressed in the linked articles are from third parties, and while they are deemed reliable, we cannot guarantee their accuracy.