If you have a large balance sitting in a non-qualified deferred compensation plan, one of the most consequential financial decisions you will ever make was probably buried in an open enrollment form you filled out years ago. Likely without a financial planner in the room, and before you had any clear picture of what your retirement income would actually look like.

Under Section 409A of the tax code, changing that election is not straightforward. And if you elected a lump sum, the tax bill that follows could be $560,000 or more in a single year.

The executives who keep the most of their deferred compensation are not the ones who earned the most. They are the ones who planned the distribution well before retirement.

Here is exactly how those decisions work, what the math looks like, and what moves are still available to you.

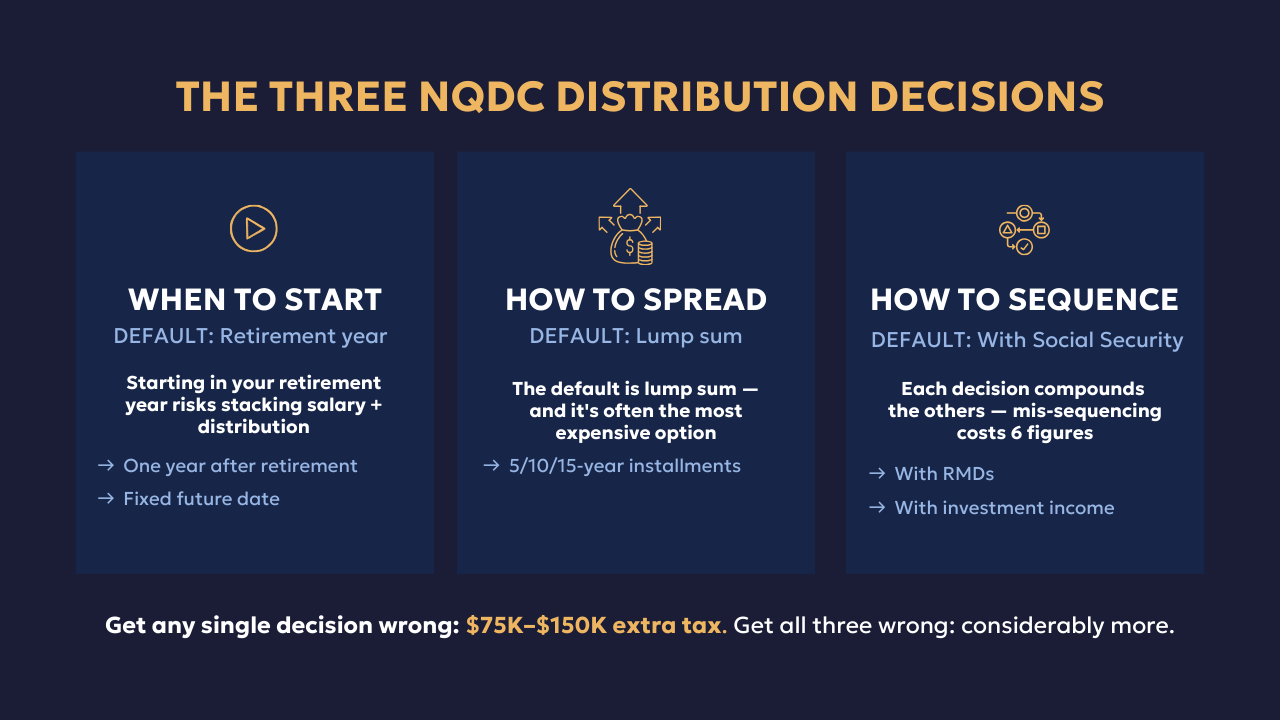

The Three Distribution Decisions That Determine Your Outcome

Most executives make three NQDC distribution decisions without fully understanding how each one compounds the others.

Decision one is when to start distributions: in your retirement year, one year after, or at a fixed future date. Decision two is how to spread them: lump sum, or 5, 10, or 15-year installments. Decision three is how to sequence your NQDC distributions alongside Social Security, required minimum distributions, and investment income.

Get any single one wrong and you are likely handing $75,000 to $150,000 back to the IRS. Get all three wrong and the number is considerably higher.

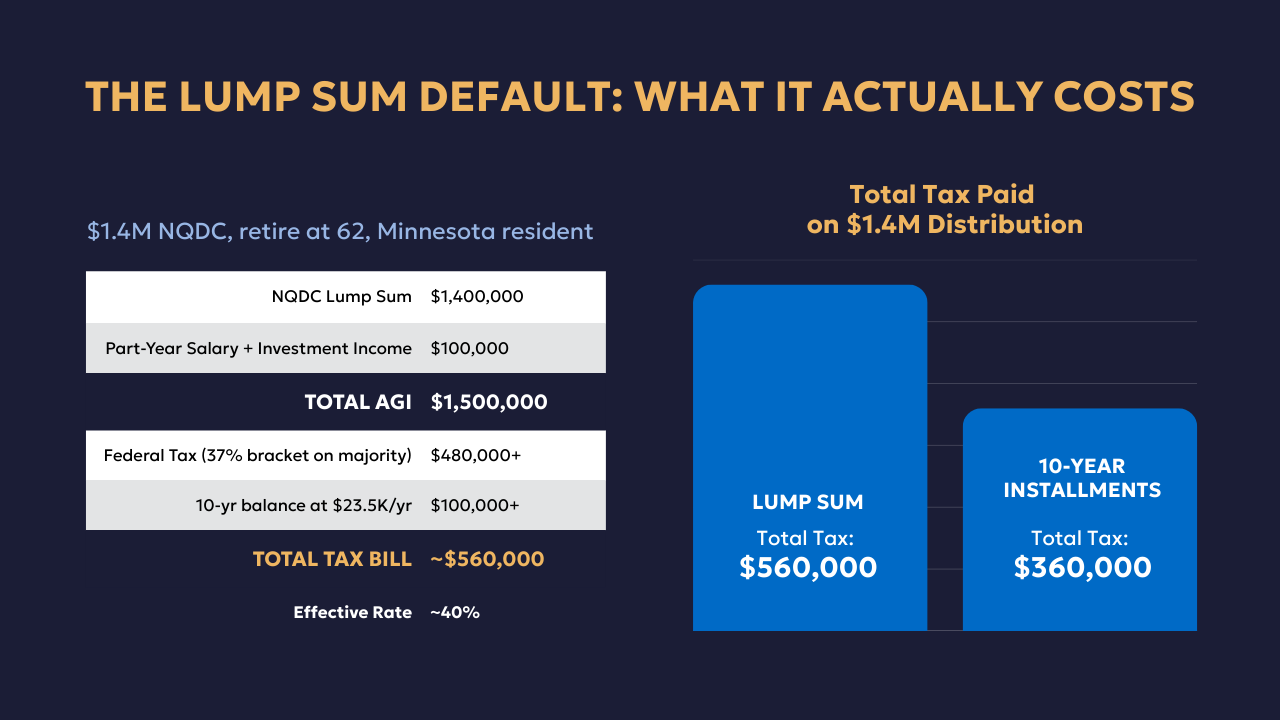

The Lump Sum Default: What It Actually Costs

The default election at most companies is a lump sum at separation from service. Most executives keep that default. Not because they modeled the tax outcome, but because the form defaulted to it and nobody flagged it.

If you retire at 62 with $1.4 million in NQDC and you elected lump sum, your year-one return includes the full distribution, any partial-year salary, investment income, and your spouse's income. In many cases that total hits $1.5 million or more in adjusted gross income. At that level in 2025, you are in the 37% federal bracket on the majority of the distribution. Add a state like Minnesota, California, or New York and your combined marginal rate on the top portion reaches 45% to 50%.

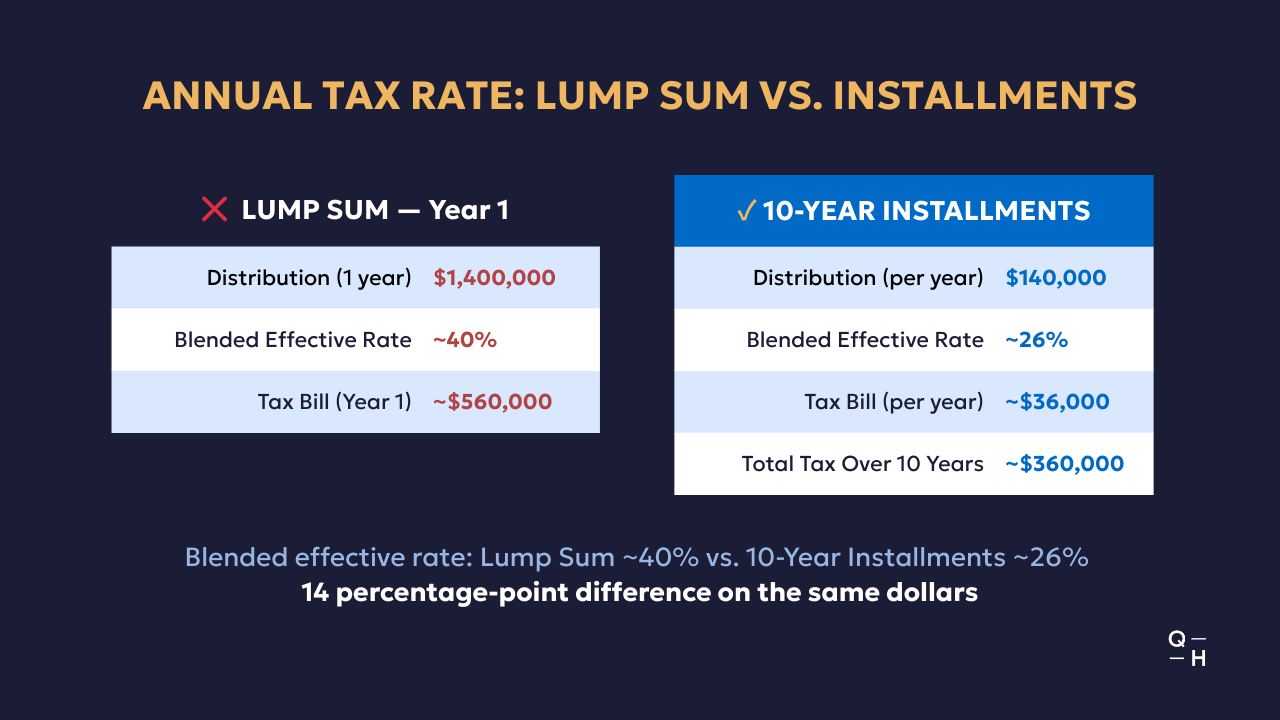

On $1.4 million at a 40% blended effective rate, the tax bill is close to $560,000 in a single year.

Now compare that to 10-year installments. At $140,000 per year with moderate other income on a joint return, your effective rate drops to the 24% to 26% range. Tax on $140,000 at a 26% blended rate is roughly $36,000 per year, or $360,000 over ten years.

Same $1.4 million. Same number of years. $200,000 different outcome. From a checkbox on an open enrollment form.

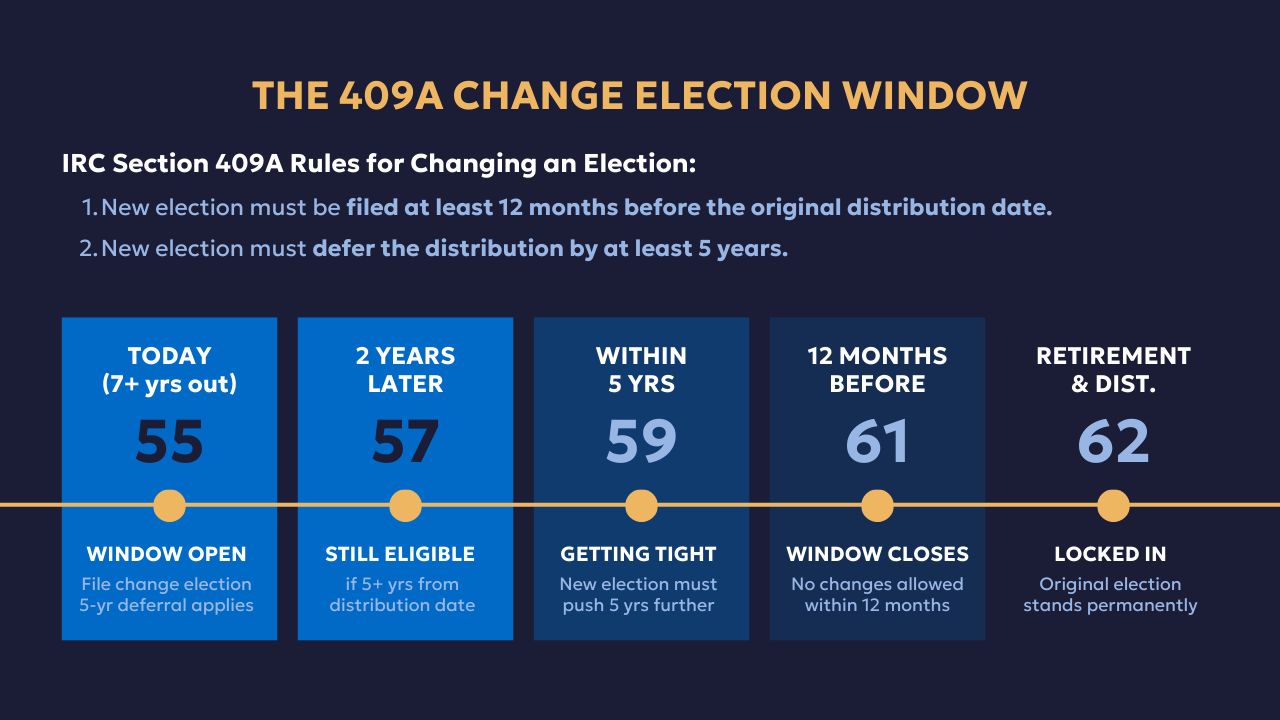

The 409A Lock and the Window Most Executives Miss

When executives hear about installment elections, the first question is usually whether they can still change theirs. Under IRC Section 409A, the answer is: not easily, and not immediately.

Two rules govern any change. The new election must be filed at least 12 months before the original distribution date. And the new election must defer the distribution by at least five years.

If you are seven or more years from retirement, this window is genuinely useful. If you are 55 and you realize your election does not work for your situation, you can file a new one today. As long as the distribution does not start for at least five years, the change is valid under 409A.

If you are two or three years out, the math gets harder. The five-year deferral may push your distribution into years you did not plan for, potentially stacking it on top of required minimum distributions in your late 60s instead of solving the problem.

The window is real. Most executives do not know it is there until after it closes.

Case Study: David and Caroline

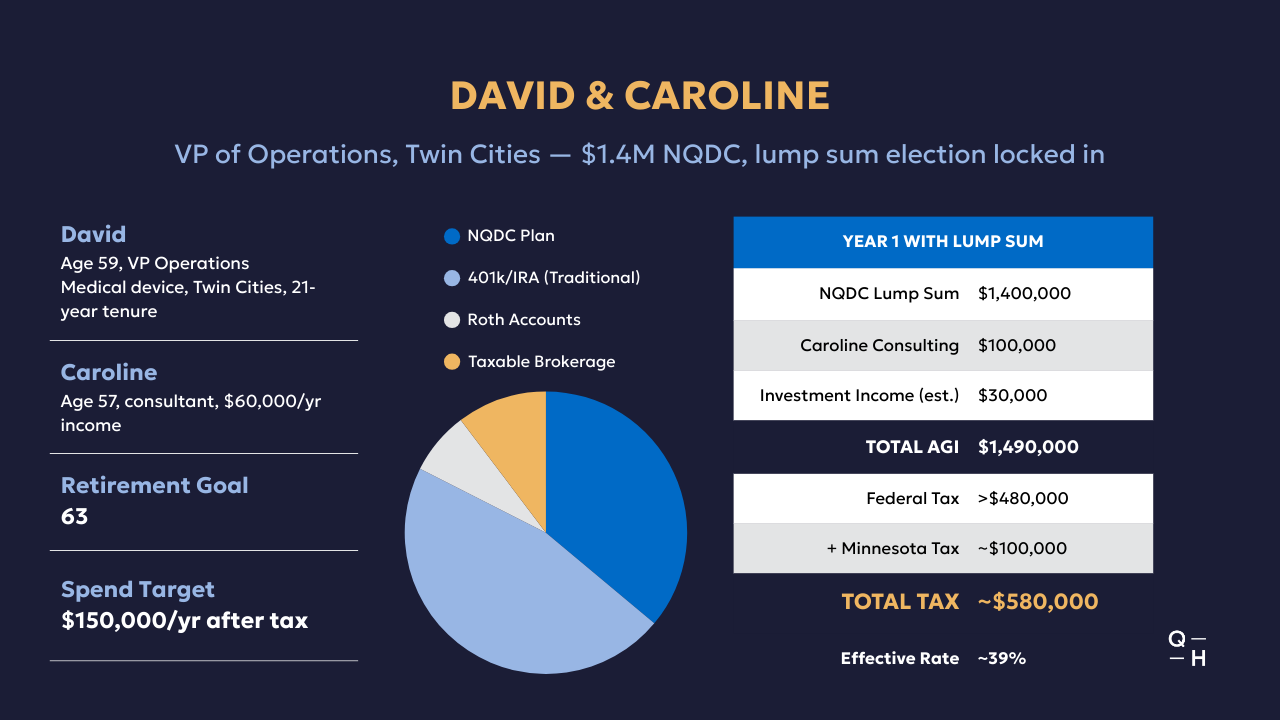

David is 59, VP of Operations at a medical device company in the Twin Cities, 21-year tenure, $1.4 million in his NQDC plan. He enrolled at 42 and kept the default lump sum election without giving it much thought.

His other assets include $1.8 million in traditional 401(k) and IRA accounts, $280,000 in Roth, and $400,000 in taxable brokerage. His wife Caroline is 57 and does consulting work at about $60,000 per year. David's plan is to retire at 63 and spend $150,000 per year after tax. They own their home outright.

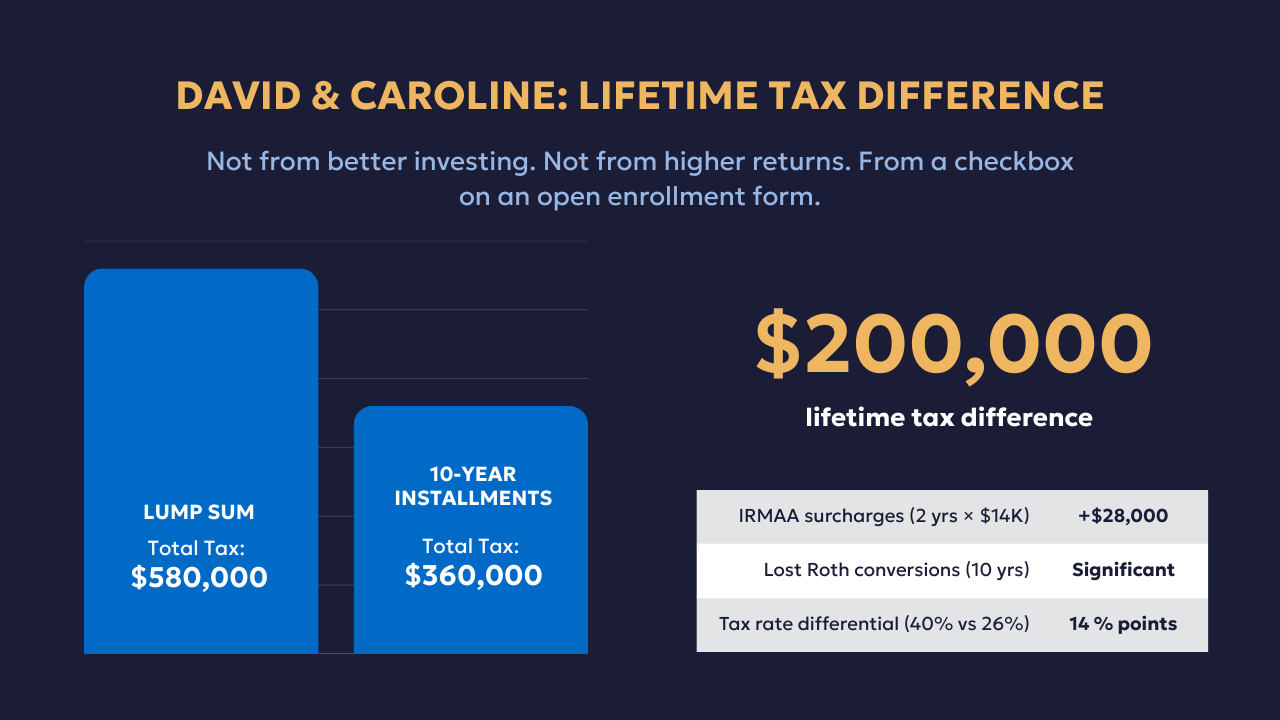

With his current election intact, year one of retirement looks like this: $1.4 million NQDC lump sum, plus $60,000 from Caroline's consulting, plus roughly $30,000 in estimated investment income. Total adjusted gross income: $1.49 million. Federal tax alone exceeds $480,000. Add Minnesota and the combined bill is close to $580,000 at an effective rate of about 39%.

But the lump sum does not just create a large tax bill. It triggers two additional problems that compound on top of each other.

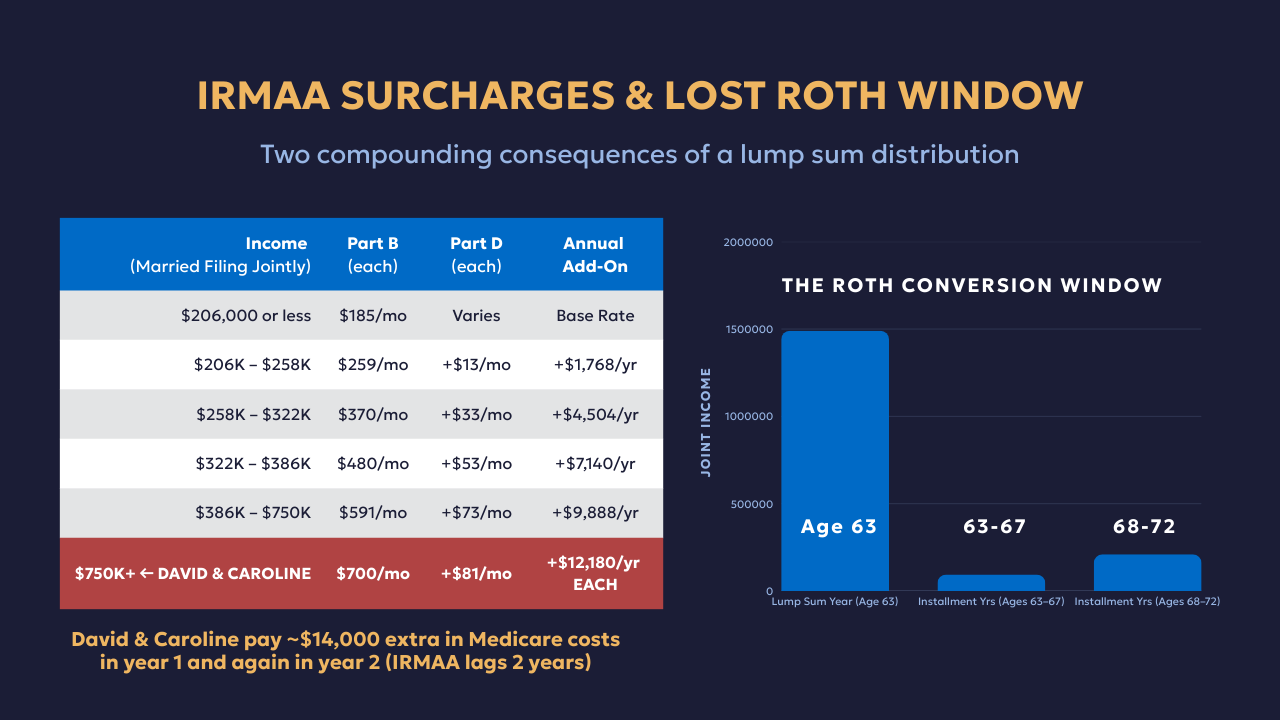

First, Medicare looks back two years to determine IRMAA surcharges. At $1.49 million in income, David and Caroline hit the highest IRMAA tier, roughly $7,000 per person per year above the base premium. That is $14,000 in additional Medicare costs, and it follows them into year two of retirement even though the distribution is gone.

Second, the Roth conversion window closes entirely. With income over $700,000, every dollar they might convert to Roth is taxed at 37% federal. They lose the most valuable Roth conversion window of their lives, the years after salary stops and before required minimum distributions begin.

Now look at what changes with 10-year installments starting one year after retirement.

Year one at age 63 has no NQDC income at all, just investment income and Caroline's consulting. Joint income runs around $90,000 to $100,000, taxed at about 22%. Starting at 68, they receive $140,000 per year in NQDC distributions plus Caroline's income, putting joint income in the $200,000 to $220,000 range at a blended effective rate of around 24%. They stay below every IRMAA surcharge threshold. And the Roth window stays open for the full first five years, allowing them to convert $80,000 to $100,000 per year at favorable rates.

The lifetime tax difference between David's current lump sum election and the installment alternative is approximately $200,000. Not from better investing. Not from different returns. From a checkbox on an open enrollment form.

Three Bracket Traps That Cost Six Figures Even With Installments

Even executives who elect installments can trigger significant tax problems if they do not sequence distributions carefully.

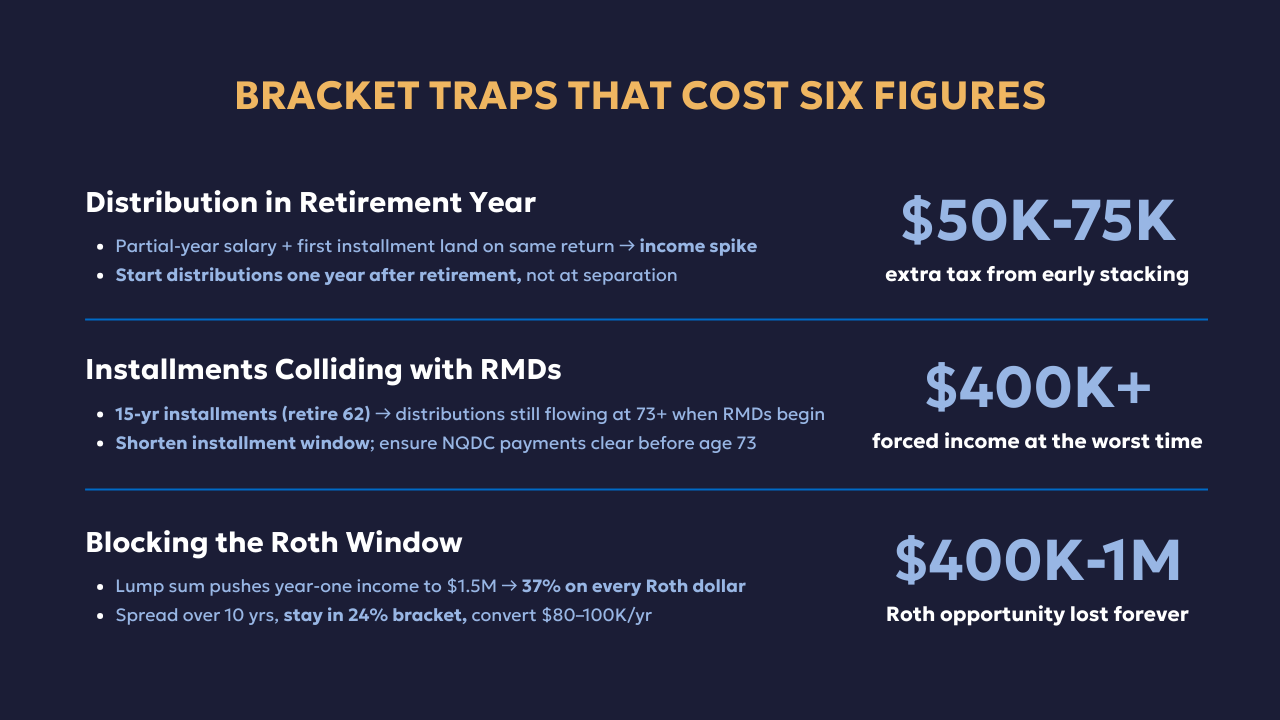

The first trap is starting distributions in your retirement year. If you retire mid-year and distributions begin at separation from service, your partial-year salary and the first installment land on the same return, creating an income spike that pushes you into a higher bracket unnecessarily. Starting distributions one year after retirement avoids this entirely.

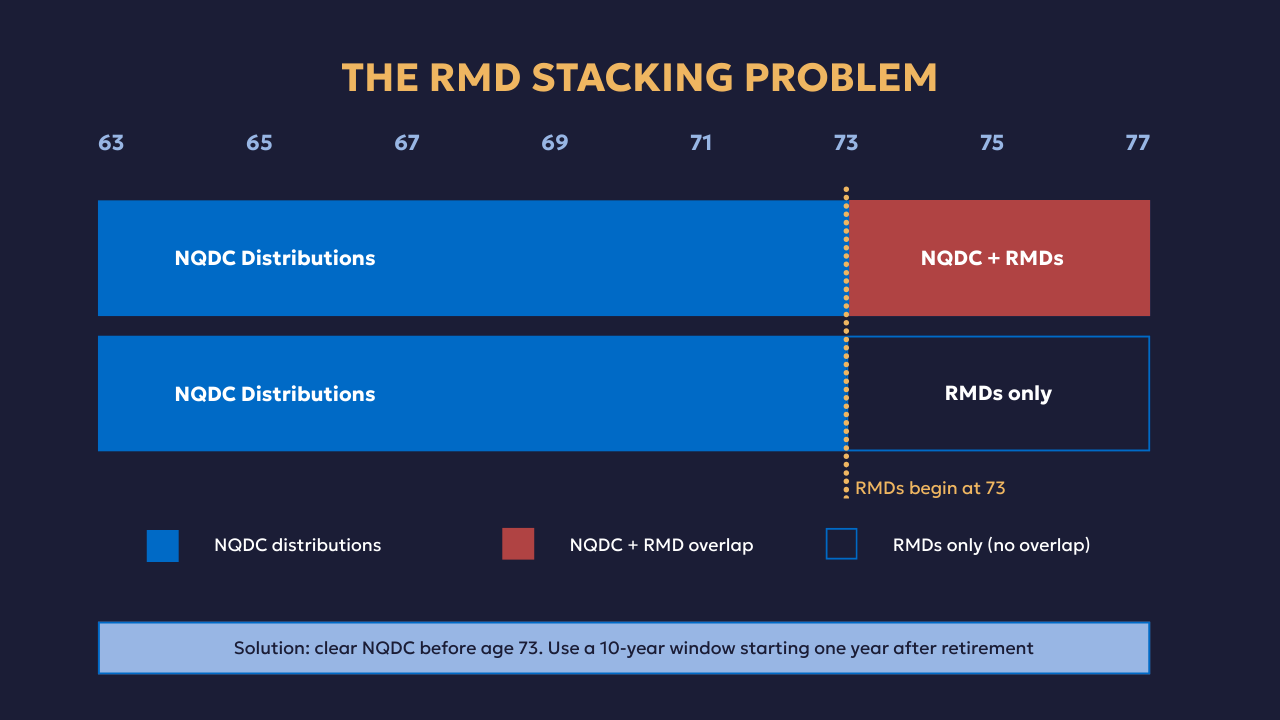

The second trap is letting installments run into your RMD years. If you retire at 62 and take 15-year installments, distributions run to age 77. Required minimum distributions start at 73. From that point forward, NQDC installments stack on top of RMDs, potentially forcing income above $400,000 at exactly the ages when you least want a tax surprise.

The solution is to shorten the installment window, start one year post-retirement, and clear the NQDC payments before your mid-70s.

The third trap is blocking the Roth conversion window. Your early 60s are often the most valuable conversion window of your life. Salary has stopped, income drops, and RMDs have not started yet. A lump sum that pushes year-one income to $1.5 million closes that window entirely. Spread over a decade at $140,000 per year, you stay under the 24% bracket and can convert $80,000 to $100,000 per year before RMDs force income you do not want.

The interaction between NQDC timing and Roth conversions is where the most sophisticated planning happens, and where the most money is saved or lost.

Four Moves if Your Election Is Already Locked In

If your election is already set and you cannot change it under 409A, there are still meaningful moves available depending on your timeline.

Move one is to file the 409A change election now if you qualify. If you are more than five years from your original distribution start date, you can still switch to installments. This window closes permanently once you are within 12 months of the distribution date. Work with a CFP who understands 409A before this option disappears.

Move two is to front-load a Donor-Advised Fund in the lump sum year. A large DAF contribution creates a dollar-for-dollar deduction against ordinary income in the same year. Contributing $150,000 to $200,000 of appreciated stock to a DAF in the lump sum year offsets that amount of NQDC income. You can still grant from the DAF to the charities you care about over time.

Move three is to retire on a timeline that creates a low-income bridge year. Retiring six months earlier than planned produces a partial-year salary situation. That calendar-year income is lower than a full year, which can reduce the total impact of a distribution landing in that same tax year.

Move four is to open the Roth conversion window in years two through five. Once the lump sum year passes and income resets, the conversion window opens. Converting aggressively from traditional IRA to Roth at 22% to 24% rates while income is lower can partially offset what was lost in the high-tax distribution year.

The Bottom Line

Your specific election, your company's plan rules, your income mix, and your state of residence all shape which of these moves is actually available to you. Every situation is different.

If you want to understand how your current NQDC elections fit into your overall retirement picture, schedule a complimentary Retirement Readiness Review. We'll do the actual analysis on your specific situation.

Ready to find out if we're the right fit for your financial planning needs? Schedule a complimentary discovery meeting where we'll provide a real assessment of how we can help your specific financial situation.

-A note from Bjorn Amundson, CFP®

This material is intended for educational purposes only. You should always consult a financial, tax, or legal professional familiar with your unique circumstances before making any financial decisions. Nothing contained in the material constitutes a recommendation for purchase or sale of any security, investment advisory services or tax advice. The information and opinions expressed in the linked articles are from third parties, and while they are deemed reliable, we cannot guarantee their accuracy.